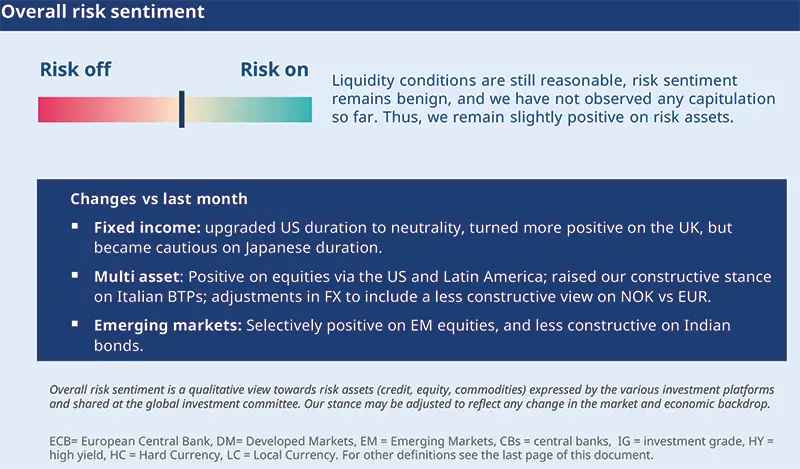

Shifting near-term narratives

Over the past few weeks, markets have been driven by higher inflation expectations, shifting central bank outlooks and contrasting news flow, all within a matter of days. This resulted in upward pressure on rates and downward pressure on risk assets in the initial part of the conflict. Most equities, including those in the US, Europe and emerging markets, have now returned close to their pre-war levels.

Efforts at ending the war and a fragile ceasefire have supported risk assets, but gains have been repeatedly tempered by a lack of resolution to the conflict and by the prospect of rates staying higher for longer. Market moves may be summarised by how the narrative has shifted between ceasefire or no ceasefire, risk-on or risk-off, and inflation and growth concerns. Looking ahead, we think:

"Central banks are vigilant, credible and flexible: anchored in inflation, alert to shocks and determined neither to overreact nor to fall behind".

Monica DEFEND

Head of Amundi Investment Institute & Chief Strategist

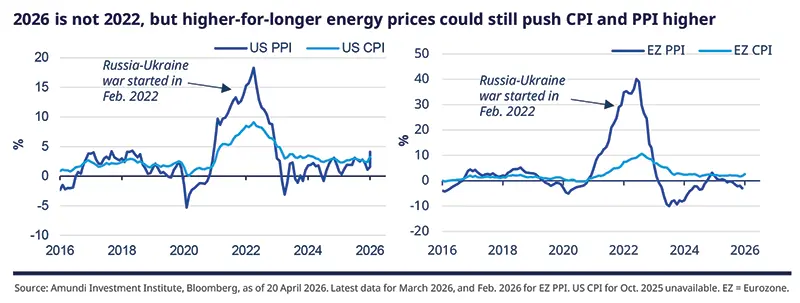

The sequencing we had in mind with respect to economic growth, energy, transport, shipping, insurance and investor/consumer confidence has been confirmed.

Usually, the hit to economic growth comes with a lag, driven by weaker real income, margin pressures, softer demand and reduced policy flexibility. Secondly, we are seeing more visible trends in the form of regional asymmetry across Europe, the US and emerging markets. Third, central banks have behaved as expected so far, and they will be cautious, reactive and not pre-emptive.

With respect to the above, what has changed over the past month?

What factors are we closely monitoring for us to change our views?

This is a time to lean on long-term convictions and, if risk assets offer an opportunity, explore areas where earnings and fundamentals are robust, while maintaining safeguards.

FIXED INCOME

Duration: less directional, more granular

Amaury D’ORSAY

Head of Fixed Income

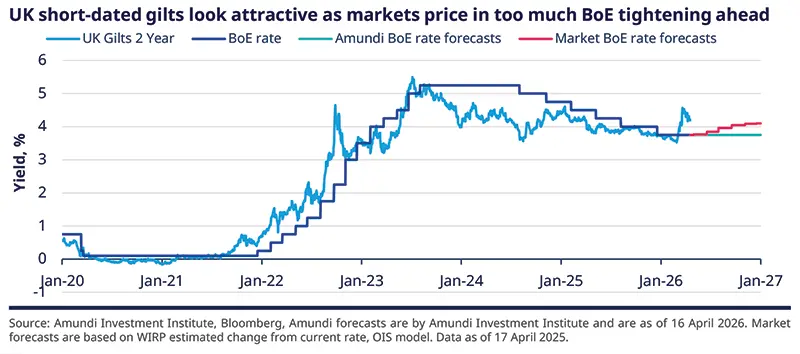

Market pricing of central bank policy decisions has changed from a slight rate cut (at the start of the war) to rate hikes now, particularly for the ECB and the BOE. While we acknowledge the concerns around inflation that have led to this repricing, we do not agree with the degree of this repricing for instance in the case of UK gilts. We also think government bonds in general could see ample supply and that could pressure yields.

Hence, instead of taking bold directional bets, we prefer to be selective across the curves and look for extra yields across corporate credit and EM. The latter has shown resilience in the face of geopolitical stress. It continues to offer strong carry, including in the high-yielding space, but one risk is of an extreme escalation in the Middle East (not our base case).

Duration and yield curves

Credit

EM bonds and FX

EQUITIES

Markets calling for a swift resolution

Barry GLAVIN

Head of Equity Platform

The massive change in behaviour of equities indicates optimism around a quick resolution of the crisis, but the actual path could be trickier, even if there is a temporary ceasefire. This crisis is not changing our structural convictions around Europe, Japan and EM (ie, Latin America, EM Asia), but we acknowledge the potential for near-term volatility. Additionally, this crisis is keeping us vigilant in exploring areas of resilience (where market moves have been excessive) around these long-term convictions.

Secondly, we now see a greater case for market dispersion rather than a single broad market direction. In Europe, we see second-round beneficiaries from the capex boost in the region and the push towards strategic autonomy. Finally, in the AI complex, markets are now rightly focused on the monetisation of investments, obsolescence risks, and EPS delivery.

Developed Markets

Emerging Markets

MULTI-ASSET

Active stance: exploit market dislocations

Francesco SANDRINI

CIO Italy & Global Head of Multi-Asset

John O’TOOLE

Global Head - CIO Solutions

As the crisis continues to evolve, we are looking ahead with an eye on risks regarding the pass-through of higher raw material costs and supply disruptions to corporate margins or consumer inflation. Long-term inflation expectations have not re-priced in a 2022-like way, suggesting that the shock is more about growth and costs than a structural shift in the inflation regime. On the market front, this allows us to remain active and tactical, particularly in areas where valuations are not better than before, and where fundamentals remain robust. Hence, we have tactically raised our stance on equities. Given the persisting geopolitical and economic risks, we think it’s an opportune time to enhance safeguards and maintain a well-diversified stance.

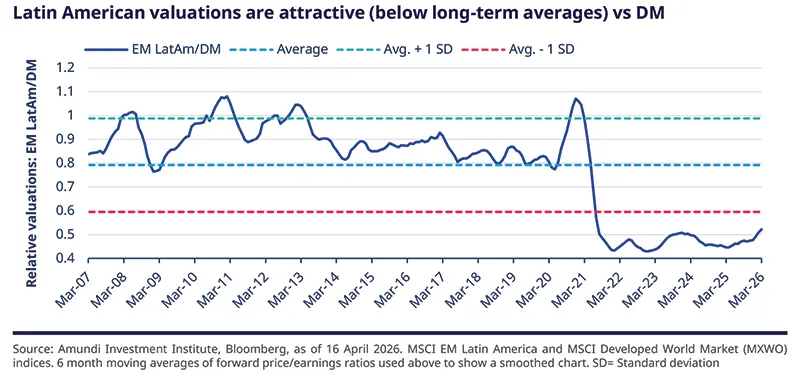

In equities, following the sharp volatility over recent weeks, we have tactically upgraded our stance on the S&P 500 and LatAm. These markets offer a more compelling risk/reward profile, are supported by resilient earnings revisions and, in the case of LatAm, show continued foreign inflows. Secondly, they do not rely on imports for their energy needs.

Duration continues to offer value, particularly for US 5Y and German bonds. Importantly, we’ve raised our constructive view on the BTP-Bund spread, which has widened materially since the Iran-related escalation, making the carry it offers even more appealing. With the Italian referendum behind us and a stable Italian government, volatility should ease and spreads should stabilise. Additionally, we see limited concerns around Italy’s deficit compared with its European peers.

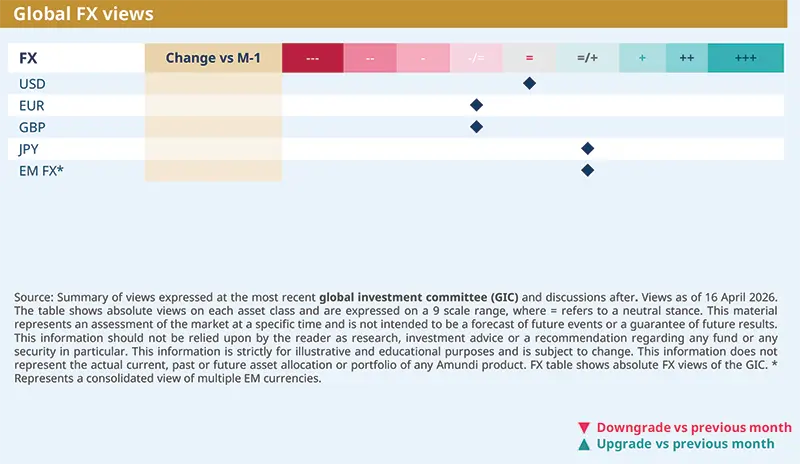

FX remains a key pillar of our multi asset views, wherein we remain cautious on the dollar from a long-term perspective. We’ve become less positive on the NOK vs the EUR following recent moves. The currency remains supported by Norway’s energy exposure, given the uncertain geopolitical environment. Additionally, we’ve rotated our positive view from EUR vs USD to AUD vs USD. Finally, we tactically downgraded EM FX to neutral.

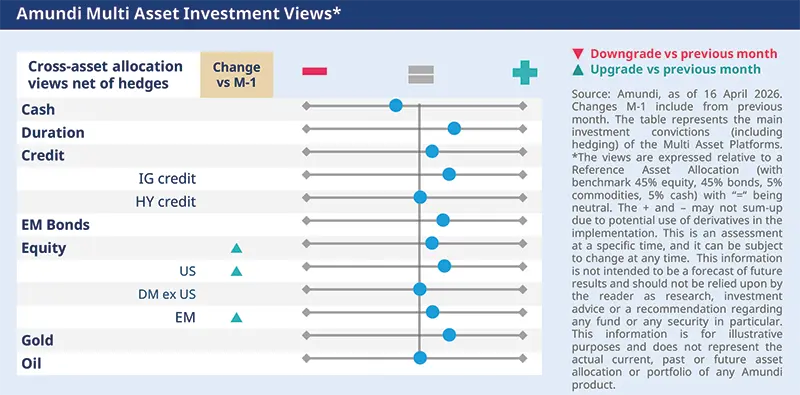

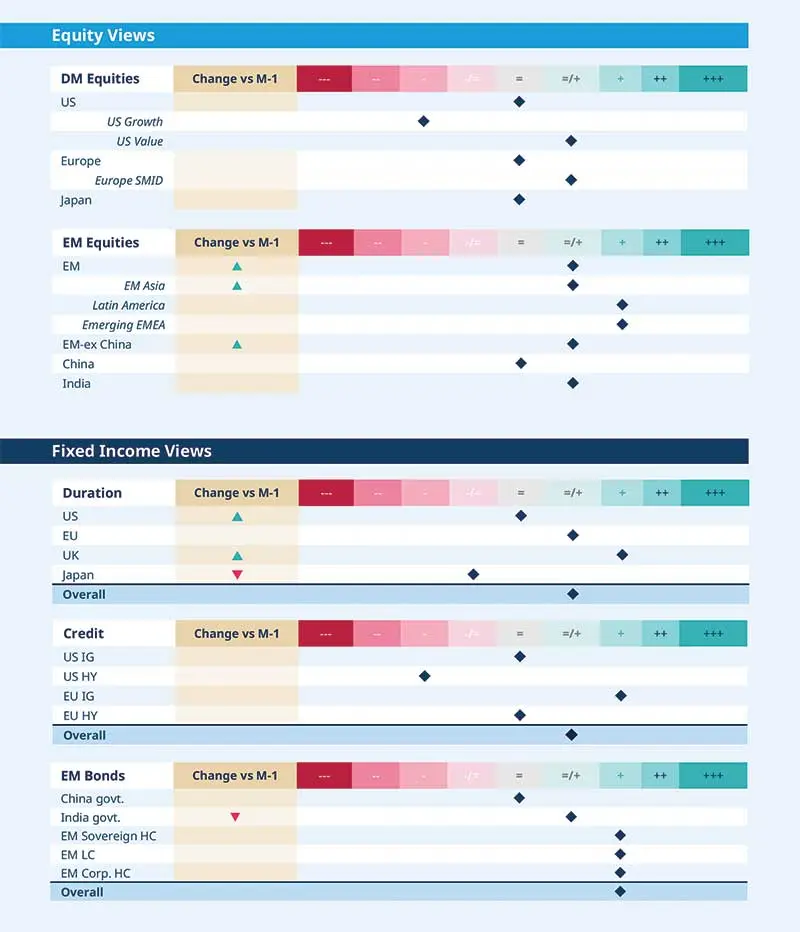

VIEWS

Amundi views by asset classes

IMPORTANT INFORMATION

The MSCI information may only be used for your internal use, may not be reproduced or disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranty of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.mscibarra.com).

The Global Industry Classification Standard (GICS) SM was developed by and is the exclusive property and a service mark of Standard & Poor's and MSCI. Neither Standard & Poor's, MSCI nor any other party involved in making or compiling any GICS classifications makes any express or implied warranties or representations with respect to such standard or classification (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such standard or classification. Without limiting any of the forgoing, in no event shall Standard & Poor's, MSCI, any of their affiliates or any third party involved in making or compiling any GICS classification have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.

This document is solely for informational purposes. This document does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or any other product or service. Any securities, products, or services referenced may not be registered for sale with the relevant authority in your jurisdiction and may not be regulated or supervised by any governmental or similar authority in your jurisdiction. The information contained in this document must not be altered or presented in a way that could give rise to misunderstanding or misrepresentation. Any use, reproduction, or distribution of the document’s content without full and proper reference to the original source is prohibited. Any information contained in this document may not be used as a basis for or a component of any financial instruments or products or indices. Furthermore, nothing in this document is intended to provide tax, legal, or investment advice. Unless otherwise stated, all information contained in this document is from Amundi Asset Management S.A.S. and is as of 23 April 2026. Diversification does not guarantee a profit or protect against a loss. This document is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The views expressed regarding market and economic trends are those of the author and not necessarily Amundi Asset Management S.A.S. or Amundi-Acba Asset Management CJSC and are subject to change at any time based on market and other conditions, and there can be no assurance that countries, markets or sectors will perform as expected. These views should not be relied upon as investment advice, a security recommendation, or as an indication of trading for any Amundi or Amundi-Acba product. Investment involves risks, including market, political, liquidity and currency risks. Furthermore, in no event shall Amundi or Amundi-Acba have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages due to its use.

Date of first use: 23 April 2026.

"AMUNDI-ACBA ASSET MANAGEMENT" CJSC is a legal entity registered in Armenia, who, based on the Investment fund management license number 0002, provided by the Central Bank of Armenia, carries out mandatory pension fund management activities in Armenia. The registered office is located 10 Vazgen Sargsyan street, Premises 100-101, Yerevan, Armenia.

For more information about Amundi-Acba you can visit www.amundi-acba.am or call 011-310-000.