Keep it turning, faster

Since the start of the year, several of the key convictions we highlighted in our outlook have been playing out, and some trends have clearly accelerated. Markets have remained well supported, with significant rotations at country, sector and stock levels.

Geopolitical fragmentation and controlled disorder remain central themes, as the recent escalation in the Middle East has shown. The situation remains fluid and, for now, is best characterised as a military shock with uncertain political ramifications. Oil prices — the principal macro transmission channel — already appear to reflect a largely temporary geopolitical risk premium.

At Davos, we heard a narrative shift, a clear break in the international order. At the Munich Security Conference, and more recently in markets, we have seen steps towards policy action. President Lagarde’s reference in her speech to the ECB’s new repo facility signifies how policymakers view the growing importance of geo‑economics.

Clearly, we are moving into a more complex market equilibrium in which policy, geopolitics and capital allocation matter as much as the economic cycle. In a fast-changing world, it is a good time to reassess our main convictions:

Our convictions are based on some of the below macro views:

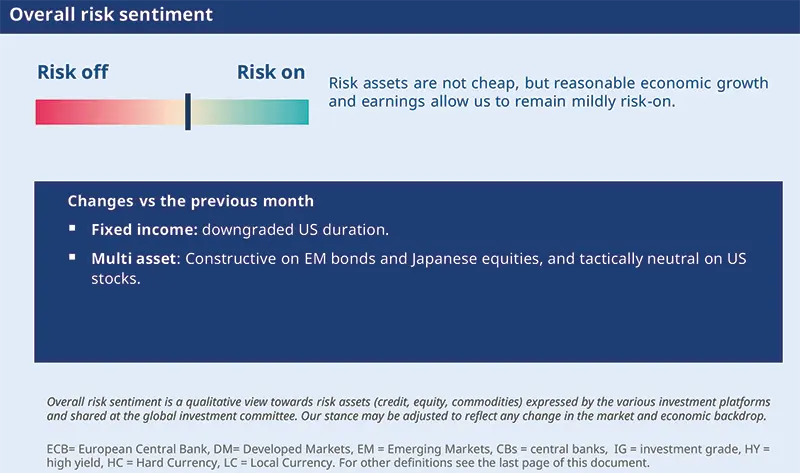

To summarise, we neither see an overheating of the economy nor a downturn this year, and maintain a moderate risk on stance. Hence, over the long term, diversification and selection look set to be better sources of returns rather than market cycles.

Our late-cycle environment allows us to keep a moderate risk-on stance, as outlined below:

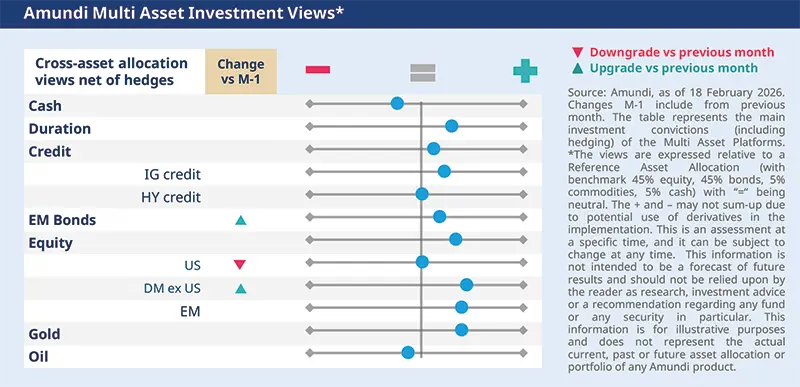

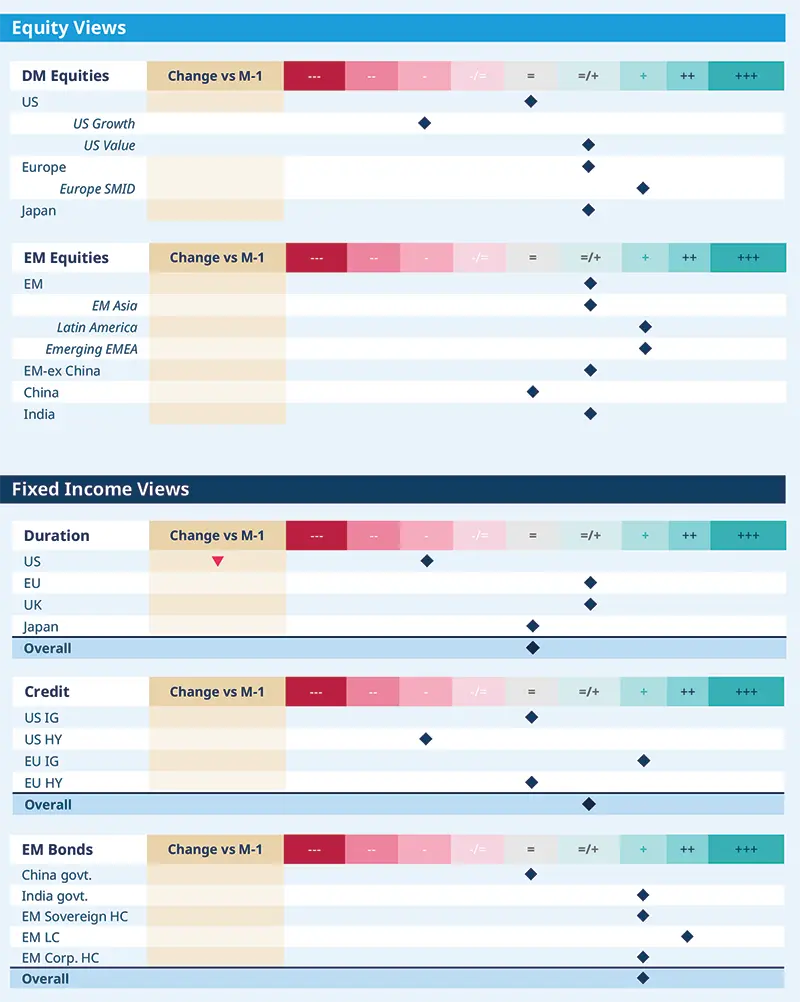

Fixed income: We are overall neutral on duration and have downgraded the US. In Japan, we have been witnessing many factors that could affect our stance. For now, we remain neutral on duration and believe the yield curve will flatten. On risk assets, we maintain a constructive view on corporate credit, and see emerging market bonds as a source of long-term returns and diversification.

Equities: We believe the volatility caused by advances in artificial intelligence is the market’s way of questioning businesses that will be disrupted by this technology. Our focus remains on identifying businesses (for instance those in the ‘real economy’) that will benefit amid this uncertainty. These include quality companies with strong balance sheets in the industrials and materials sector. We are also positive on consumer staples. Strong growth persists in emerging markets, although there are divergences across regions. We are positive on Latin America and Emerging Europe.

Multi asset: We keep a flexible approach across asset classes to identify areas of value, which we now also see in EM bonds due to their robust carry and diversification potential. Also, we are now optimistic on Japanese equities, due to strong earnings growth prospects, but neutral on US equities. Overall, we maintain a well-diversified stance.

FIXED INCOME

Rates to remain range bound

Amaury D’ORSAY

Head of Fixed Income

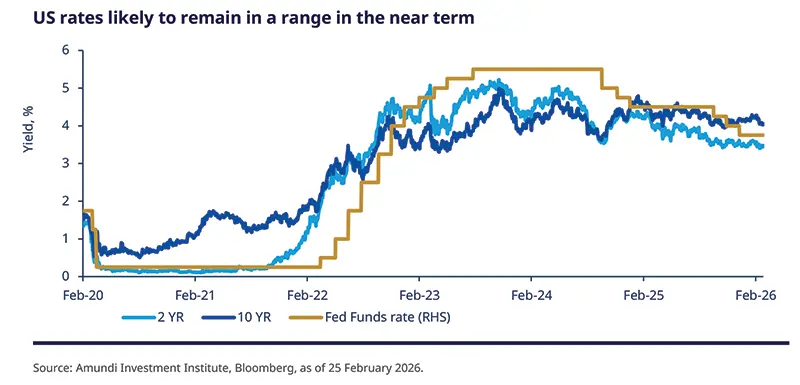

We believe that, while disinflation will continue in the US, the overall inflation will remain between 2.5% and 3% this year, which is above the Fed target. Hence, in the very near future the Fed is likely to remain on hold. Around mid-year, when there is more visibility on inflation, the Fed may reduce rates.

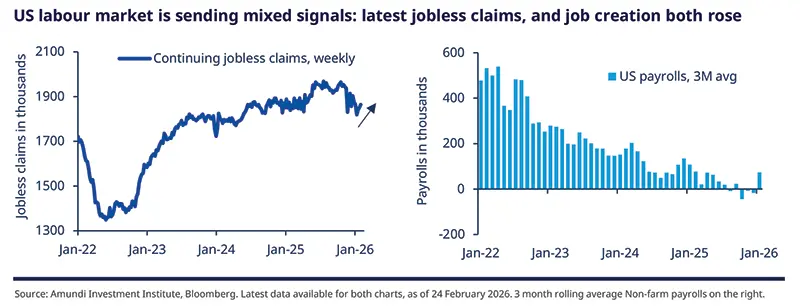

At the same time, we don’t see Fed pivoting towards a rate hike, because labour markets are not giving any clear indication of improvement. Overall, rates will remain range-bound. In Asia, Japan is an outlier, and we are monitoring how the fiscal/monetary policies evolve. Overall, we stay balanced, with slightly positive views on corporate credit, EM bonds and a selective stance on duration across DM.

Duration and yield curves

Credit and EM bonds

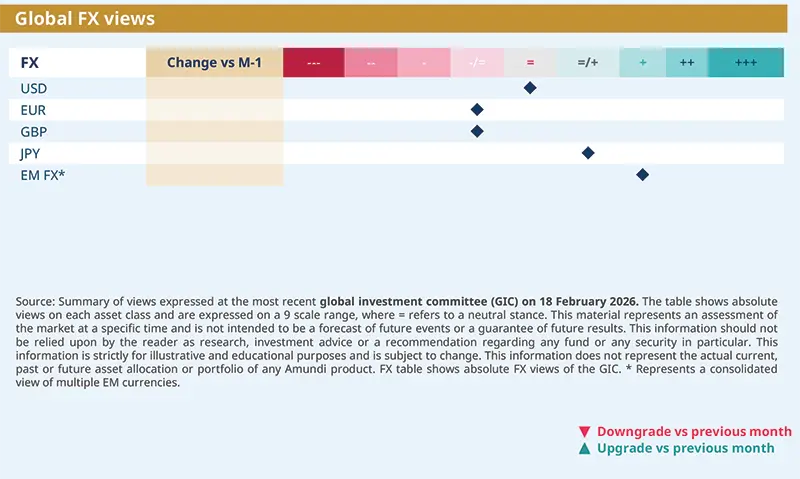

FX

EQUITIES

AI disruption may support rotation

Barry GLAVIN

Head of Equity Platform

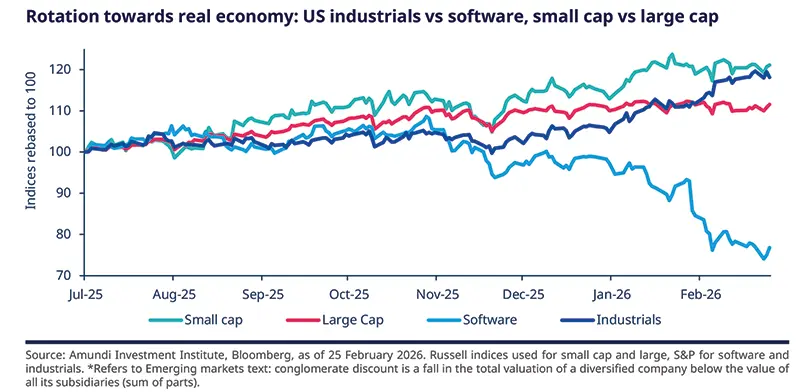

The global macro environment is decent, but tariffs have again created uncertainty in this world of controlled disorder. On the market front, volatility in equity markets, including in AI segments, is a reminder of the bona fide questions the market will ask about these companies' competitive moats and their earnings potential. Any progress on this – for example, the development of a new AI model – could result in increased volatility for companies whose business models are at risk of disruption.

We could witness a general trend favouring high-quality companies in industrials versus losers in the technology segments. Our focus remains on building a fundamental view on businesses that could sustain this rotation, and may even benefit from it, particularly in Europe, Japan and EM.

Developed Markets

Emerging Markets

MULTI-ASSET

Explore the carry potential in EM

Francesco SANDRINI

CIO Italy & Global Head of Multi-Asset

John O’TOOLE

Global Head - CIO Solutions

The growth momentum is stronger than expected in the US and Europe, with irregular progress towards the inflation target that could lead the Fed and ECB to stay on hold in the near term. In Japan, PM Sanae Takaichi’s victory gives an additional push to her “Sanaenomics” agenda that could revamp Japan’s growth potential. Elsewhere, EM show improving financial conditions that could improve their economic pattern. In this context, we have recalibrated our stance to explore carry in EM, maintaining a modestly pro-risk stance.

While we remain positive on equities through Europe and UK, we have tactically adopted a neutral stance on the US. Concentration risk in the tech sector remains elevated, and there is rising demand for diversification beyond crowded trades. Secondly, we upgraded Japan due to expectations of strong earnings growth and an improvement in return on equity. We remain constructive on emerging markets in general and specifically on LatAm.

On FI, we have become positive on EM spreads, which should benefit from a risk-on sentiment. Although geopolitical risks persist and valuations are tight, EM spreads are supported by ample liquidity, positive macro momentum and attractive carry. In DM, we stay positive on EU IG. On govt. bonds, we are overall constructive on the US and EU. But now we prefer to express our view on the EU through German bunds, rather than EMU swaps. Bund valuations vs swaps are attractive and should gain from potential dovishness from the ECB and provide a safeguard in a risk-off scenario. We also remain positive on Italian BTPs.

We turned positive on a basket of EM FX (TRY, BRL, HUF etc. against the USD), as it provides a diversified EM exposure and should benefit from positive EM growth and a weaker dollar. In commodities, we are constructive on gold, but cautious on oil. In addition, owing to the recent equities rally and persistent geopolitical risks, we think it’s essential to strengthen safeguards, particularly on US equities.

VIEWS

Amundi views by asset classes

IMPORTANT INFORMATION

The MSCI information may only be used for your internal use, may not be reproduced or disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranty of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.mscibarra.com).

The Global Industry Classification Standard (GICS) SM was developed by and is the exclusive property and a service mark of Standard & Poor's and MSCI. Neither Standard & Poor's, MSCI nor any other party involved in making or compiling any GICS classifications makes any express or implied warranties or representations with respect to such standard or classification (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such standard or classification. Without limiting any of the forgoing, in no event shall Standard & Poor's, MSCI, any of their affiliates or any third party involved in making or compiling any GICS classification have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.

This document is solely for informational purposes. This document does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or any other product or service. Any securities, products, or services referenced may not be registered for sale with the relevant authority in your jurisdiction and may not be regulated or supervised by any governmental or similar authority in your jurisdiction. The information contained in this document must not be altered or presented in a way that could give rise to misunderstanding or misrepresentation. Any use, reproduction, or distribution of the document’s content without full and proper reference to the original source is prohibited. Any information contained in this document may not be used as a basis for or a component of any financial instruments or products or indices. Furthermore, nothing in this document is intended to provide tax, legal, or investment advice. Unless otherwise stated, all information contained in this document is from Amundi Asset Management S.A.S. and is as of 28 february 2026. Diversification does not guarantee a profit or protect against a loss. This document is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The views expressed regarding market and economic trends are those of the author and not necessarily Amundi Asset Management S.A.S. or Amundi-Acba Asset Management CJSC and are subject to change at any time based on market and other conditions, and there can be no assurance that countries, markets or sectors will perform as expected. These views should not be relied upon as investment advice, a security recommendation, or as an indication of trading for any Amundi or Amundi-Acba product. Investment involves risks, including market, political, liquidity and currency risks. Furthermore, in no event shall Amundi or Amundi-Acba have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages due to its use.

Date of first use: 28 February 2026.

"AMUNDI-ACBA ASSET MANAGEMENT" CJSC is a legal entity registered in Armenia, who, based on the Investment fund management license number 0002, provided by the Central Bank of Armenia, carries out mandatory pension fund management activities in Armenia. The registered office is located 10 Vazgen Sargsyan street, Premises 100-101, Yerevan, Armenia.

For more information about Amundi-Acba you can visit www.amundi-acba.am or call 011-310-000.