Diverging market signals

Over the past month, stock and bond markets have been driven by diverging forces. Bond yields have risen at the short end due to inflation pressures and more hawkish central banks, while long-end yields have climbed on higher term premiums amid Middle East uncertainty and ongoing high fiscal deficits.

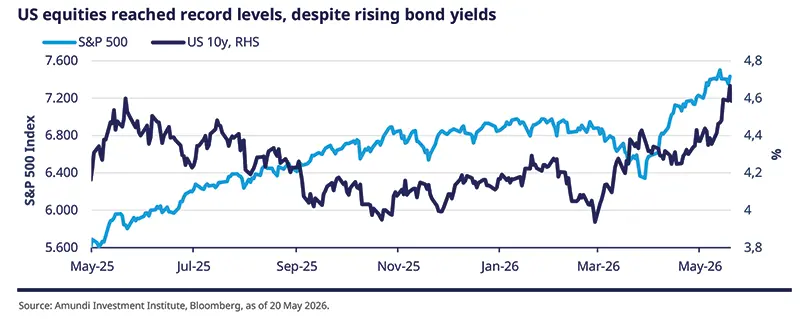

Equities, however, have been less affected by the war. Markets rebounded from their March lows, although the rally has been largely driven by a few themes (energy, hyperscalers, memory chips), a handful of artificial intelligence-linked (AI) names and the prospect of productivity gains, which we think will only happen over the long term.

To us, the diverging narratives between bonds and equities signal the difficulty of assessing the impact of disruption to traffic flow through the Strait of Hormuz. In addition, it highlights the uncertainty around second-round economic effects – the transmission of the crisis from energy and logistics to inflation, growth, corporate margins and business and consumer confidence.

To conclude, it is important to note that the Middle East shock should now be treated as an ongoing risk regime, rather than a temporary event. The key question going forward is whether the shock will remain manageable or develop into a macro-financial shock.

Hence, uncertainty remains high, reinforcing the need to closely monitor the economic fallout to assess the next allocation move. For now, with liquidity and fundamentals supportive of risky assets, we maintain a cautious risk-on stance, with enhanced protections.

Amundi Investment Institute: Signal of change to central banks’ reaction functions

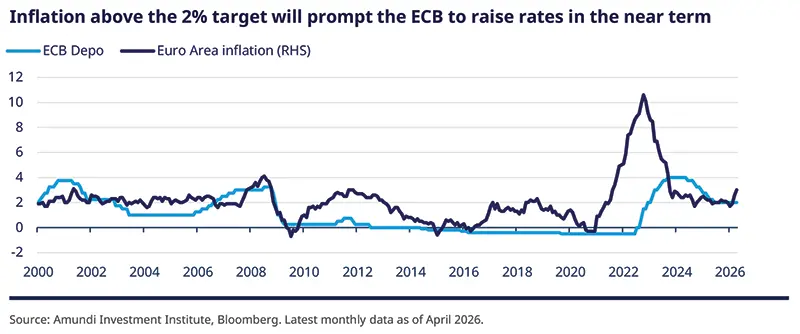

Central banks turned more hawkish in their latest meetings. A smooth easing cycle is no longer the base case this year, but an easing bias may return later if inflation falls to target. For the ECB, we now expect two hikes of 25 bps this year but rule out a full hiking cycle. For the Bank of England (BoE), one hike by the end of 2026 is projected, and we have postponed our easing bias to Q2 2027 as the UK’s inflation profile remains uncomfortable in the near term. The Fed is currently in observation mode and, looking ahead, we expect it to remain on hold for a prolonged period of time, with cutting not be resumed before Q2 2027, when the disinflationary trend will become more visible. For the BoJ, we continue to expect a rate hike in June this year and have added a second move higher in Q4 2026 that will narrow the real rate gap with other developed markets.

Emerging markets monetary policy divergence will increase. Vulnerable energy importers, including India, have limited room to cut (despite softer growth momentum) as oil sensitivity, foreign exchange pressure and inflation credibility will matter more. The People’s Bank of China should remain supportive but focused on liquidity and credit support rather than aggressive rate cuts.

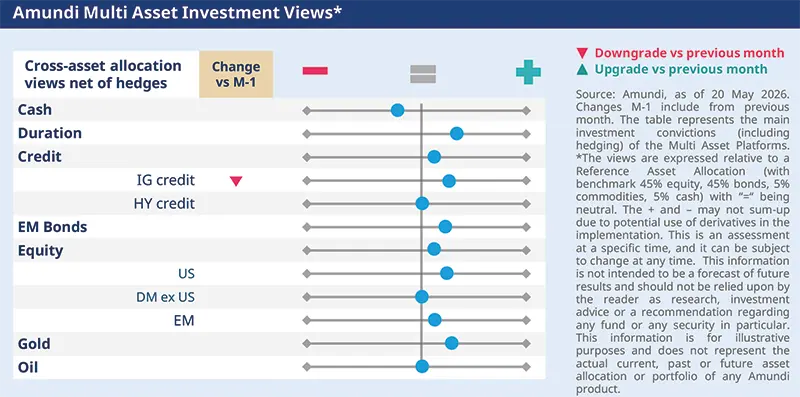

Against a backdrop of solid earnings growth, contained stress and reasonable market liquidity, we remain slightly pro-risk. Our convictions across asset classes are outlined below:

FIXED INCOME

Shifting rate dynamics amid inflation

Amaury D’ORSAY

Head of Fixed Income

Since the beginning of the Iran war, bond markets have come under pressure from a combination of factors. Inflationary pressures have started to re-emerge, pushing short-term rates higher, while fears that weaker growth and higher support measures will weigh on public finances and bond supply have put upward pressure on long-term rates.

These inflation pressures are making central banks (ECB, BoE) a bit more hawkish. We believe these banks could raise rates, but without starting a hiking cycle. Hence, we remain positive on duration overall but are applying a more selective lens across geographies and yield curves. Additionally, we maintain our overall curve steepening views but acknowledge higher near-term uncertainty due to ambiguity over monetary policy actions.

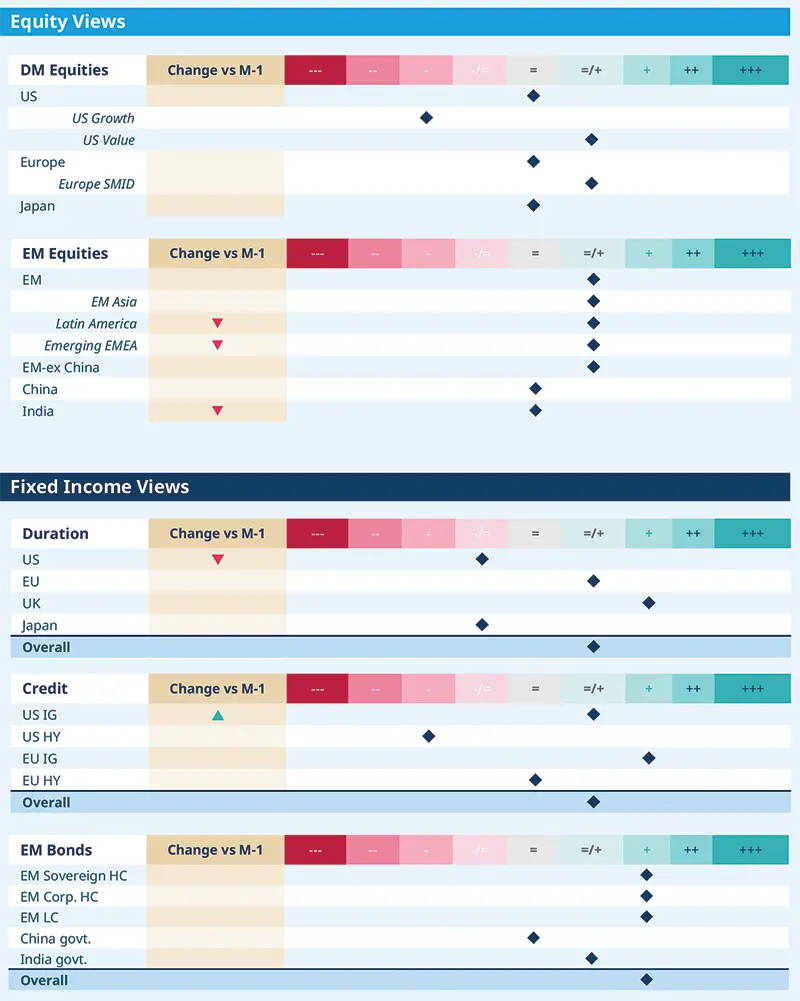

Duration and yield curves

Credit

EM bonds and FX

EQUITIES

Global opportunities, greater resilience

Barry GLAVIN

Head of Equity Platform

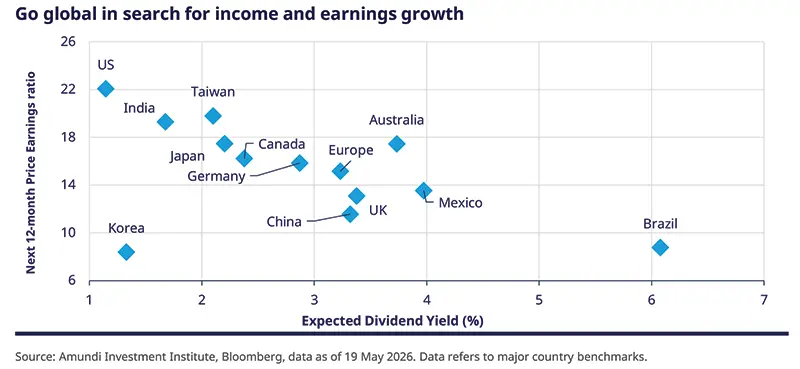

The market rally has been driven by lower oil prices, Middle East deal expectations and AI-related tech earnings. However, commodity shortages are likely to persist and inflationary pressures will remain elevated in the near term. Hence, our focus remains on businesses that can deliver strong earnings and pass on these higher costs to consumers in order to preserve margins. We are exploring such companies with a global view, particularly in Japan (reflation story), Europe and the emerging markets.

While sentiment in some of these regions has been weakened owing to their reliance on energy imports, the long-term case is intact. In Europe, this crisis will push the region towards achieving strategic autonomy and strengthening energy security as well as supply chains in the long run.

Developed Markets

Emerging Markets

MULTI-ASSET

Mildly risk-on, with enhanced protections

Francesco SANDRINI

CIO Italy & Global Head of Multi-Asset

John O’TOOLE

Global Head - CIO Solutions

The growth outlook remains reasonable, although there are signs of divergences between the US and Europe, as well as expectations of above-target inflation in most DM. These inflation concerns are more evident in fixed income. Risk assets, on the other hand, have been driven higher by strong corporate earnings, the AI story, and optimism around a resolution to the Middle East conflict. We remain mildly pro-risk, seizing opportunities created by market moves and a greater need to strengthen hedges.

In equities, while we remain mildly positive on risk through US and EM Latin equities, we acknowledge the recent record levels that markets have reached. We believe the risks (geopolitics, US-Iran) that markets are shrugging off remain present. Hence, investors should consider increasing protection on US equities and maintain safeguards in Europe.

In bonds, we remain positive on US duration, German govies and Italian BTPs vs Bunds and on EM spreads. But we are cautious on JGBs. In EU IG credit, where we are very active, we have tactically reduced our stance following recent spread tightening. We remain constructive in the segment due to attractive carry and robust fundamentals. We will continue to look for opportunities to upgrade our views when valuations improve.

In FX, we like commodity-linked and higher-yielding currencies such as AUD and NOK. We have also tactically trimmed our constructive stance on the JPY vs CHF. Negative real rates in Japan could pressure the yen in the near term. But recent BOJ interventions indicate the central bank’s intention to cap yen weakness. The currency’s attractive valuation (vs the Swiss franc) and policy divergence (rate cuts in Switzerland and hikes by BOJ) are other supporting factors. Finally, over the long term, gold should benefit amid geopolitical risks and central bank purchases.

VIEWS

Amundi views by asset classes

IMPORTANT INFORMATION

The MSCI information may only be used for your internal use, may not be reproduced or disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranty of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.mscibarra.com).

The Global Industry Classification Standard (GICS) SM was developed by and is the exclusive property and a service mark of Standard & Poor's and MSCI. Neither Standard & Poor's, MSCI nor any other party involved in making or compiling any GICS classifications makes any express or implied warranties or representations with respect to such standard or classification (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such standard or classification. Without limiting any of the forgoing, in no event shall Standard & Poor's, MSCI, any of their affiliates or any third party involved in making or compiling any GICS classification have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.

This document is solely for informational purposes. This document does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or any other product or service. Any securities, products, or services referenced may not be registered for sale with the relevant authority in your jurisdiction and may not be regulated or supervised by any governmental or similar authority in your jurisdiction. The information contained in this document must not be altered or presented in a way that could give rise to misunderstanding or misrepresentation. Any use, reproduction, or distribution of the document’s content without full and proper reference to the original source is prohibited. Any information contained in this document may not be used as a basis for or a component of any financial instruments or products or indices. Furthermore, nothing in this document is intended to provide tax, legal, or investment advice. Unless otherwise stated, all information contained in this document is from Amundi Asset Management S.A.S. and is as of 29 May 2026. Diversification does not guarantee a profit or protect against a loss. This document is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The views expressed regarding market and economic trends are those of the author and not necessarily Amundi Asset Management S.A.S. or Amundi-Acba Asset Management CJSC and are subject to change at any time based on market and other conditions, and there can be no assurance that countries, markets or sectors will perform as expected. These views should not be relied upon as investment advice, a security recommendation, or as an indication of trading for any Amundi or Amundi-Acba product. Investment involves risks, including market, political, liquidity and currency risks. Furthermore, in no event shall Amundi or Amundi-Acba have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages due to its use.

Date of first use: 29 May 2026.

"AMUNDI-ACBA ASSET MANAGEMENT" CJSC is a legal entity registered in Armenia, who, based on the Investment fund management license number 0002, provided by the Central Bank of Armenia, carries out mandatory pension fund management activities in Armenia. The registered office is located 10 Vazgen Sargsyan street, Premises 100-101, Yerevan, Armenia.

For more information about Amundi-Acba you can visit www.amundi-acba.am or call 011-310-000.