Space dreams versus Earth reality

Over the last month, central banks have taken an increasingly hawkish turn that has forced markets to start reassessing the AI trade’s remarkable momentum. As inflation continues to rise, policymakers have remained cautious despite positive headlines around a US/Iran ceasefire deal.

Optimism around the AI trade has been the main driver of risk assets, with momentum stocks leading. But due to rising uncertainty on potential future hikes, markets have started to question whether AI’s elevated valuations can remain justified, particularly in a more uncertain interest-rate environment with increasing IPO supply. Rotations have already started to materialise, as investors take profits and broaden exposure into less crowded areas of the market.

Looking ahead, concerns around AI profitability, valuations and concentration risks are likely to persist. Capex overspending and lacklustre results remain key risks for US hyperscalers, especially as the recent rally in memory-chip makers may be showing signs of excess. Well-backed IPOs can help support the market, but more players and more metrics for assessing the AI space will increase the scrutiny of current leaders and could drive broader diversification. Against this backdrop, we still see growth holding, but not strongly enough to offset rising macro costs and broadening price pressures.

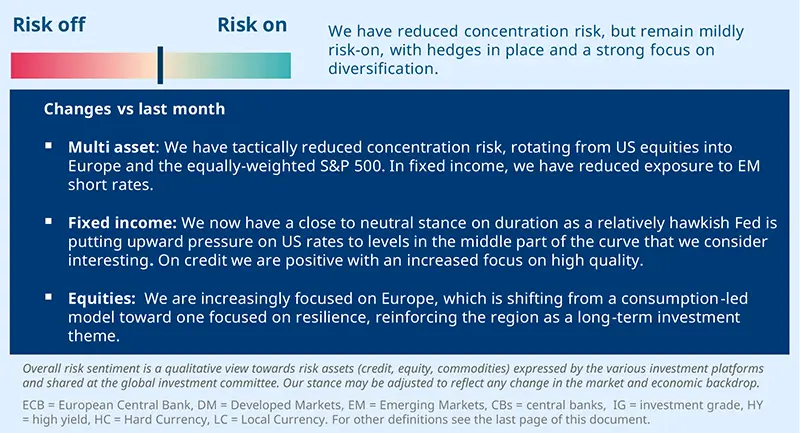

In conclusion, the less benign economic backdrop is, for now, offset by liquidity and solid earnings growth. We therefore maintain a cautious risk-on stance, recently further trimmed down, with hedges in place and a focus on diversification away from concentration risk.

Overall, in assessing where to invest, we should look beyond short-term headlines and focus on structural resilience, pricing power, and the ability of companies to absorb shocks — qualities that can be found across regions and sectors. Our convictions across asset classes are outlined below:

FIXED INCOME

Balancing inflation and growth risks

Amaury D’ORSAY

Head of Fixed Income

Under a “fragile de-escalation" scenario, inflation is likely to remain above central banks’ targets for longer, with rising risks of second-round effects, particularly in Europe, where the growth outlook remains fragile. In the EU, in particular, we think markets are currently underestimating growth risks and, consequently, we do not expect a full-fledged hiking cycle by the central banks (ECB, BOE), which makes the short end of the curves attractive

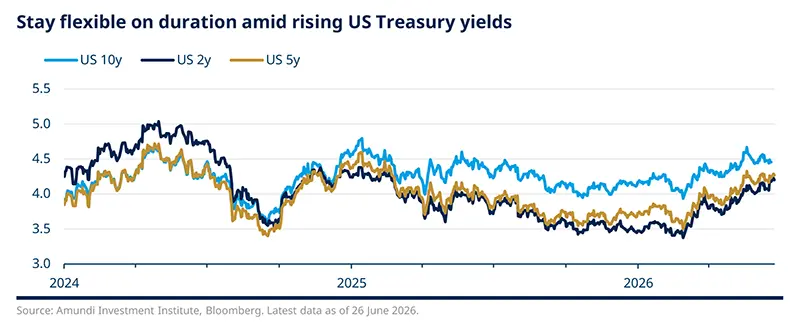

In the US, robust labour data, high headline inflation and a relatively hawkish Fed are putting upward pressure on US rates, to levels that we consider interesting in the middle part of the curve.

Duration and yield curves

Credit

EM bonds and FX

EQUITIES

An industrial play for Europe

Barry GLAVIN

Head of Equity Platform

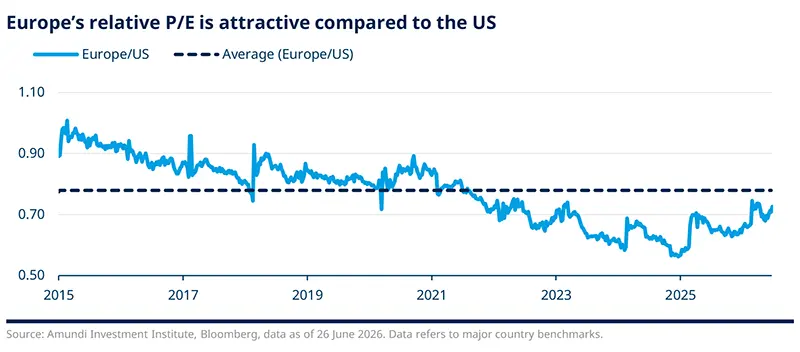

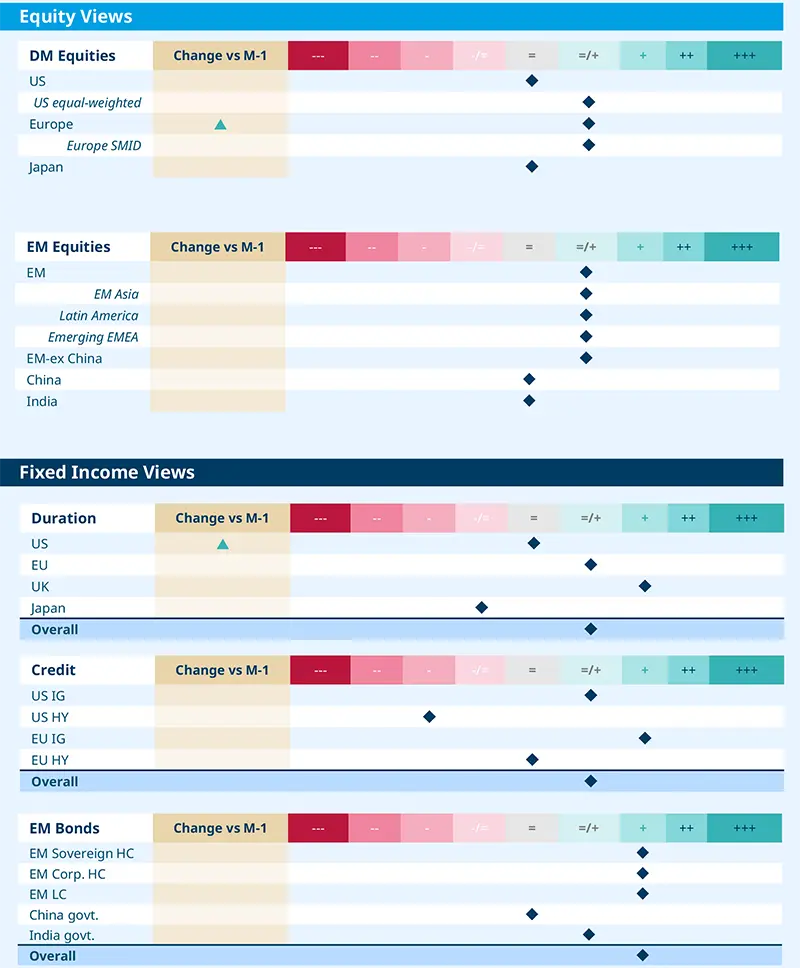

Markets have remained supported by earnings growth, helping to offset concerns over rising US yields. Looking ahead, monetary policy actions and policy stance will be key factors to monitor. Strategically, we continue to see high valuation and concentration risks in the US. Hence, we favour Europe, Japan and EM. Europe, in particular, is shifting from a consumption-led model toward one focused on resilience, reinforcing the region as a long-duration investment theme.

In Japan, the equity market outlook remains constructive, with earnings momentum driven by banks and AI-related stocks. Emerging markets are also supported by their appeal as a source of diversification amid geopolitical and economic uncertainty.

Developed Markets

Emerging Markets

MULTI-ASSET

Mildly pro-risk, with an emphasis on selectivity

Francesco SANDRINI

CIO Italy & Global Head of Multi-Asset

John O’TOOLE

Global Head - CIO Solutions

May was positive for risk assets, but the macro backdrop weakened slightly. Growth is becoming more uneven while inflation is showing more clearly in the data across the US, the Euro Area and the UK, leaving central banks less comfortable. Against this backdrop, the tone remains mildly pro-risk, with greater selectivity.

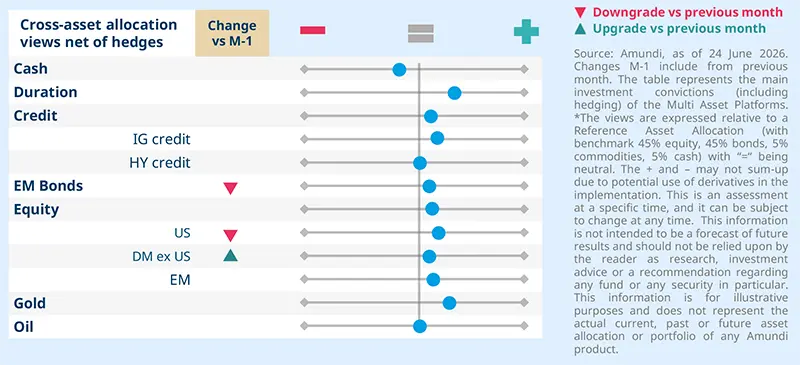

We remain mildly positive on equities, supported by strong earnings, but have reduced concentration risk by lowering our exposure to US equities and diversifying into Europe and the equally-weighted S&P 500. European equities remain under-owned and have lagged the US, but we see potential for a rebound in H2. Given persistent uncertainty, we continue to maintain protection on the US and the Euro Area.

In fixed income, we remain long US 5-year duration, as this part of the curve still looks attractive. In Europe, we maintain a long-duration bias via Bunds and Schatz. While the ECB is likely to hike rates once more this year, we think it would not completely ignore weakening consumption and growth. In Euro peripherals, BTPs remain attractive, as Italy still appears comparatively stable. However, we remain short 10-year JGBs, given Japan’s policy normalisation, higher energy costs, yen weakness and rising inflation risks. Finally, we remain constructive on EU IG credit, given attractive valuations, demand from yield buyers and positive seasonality. On EM, we have reduced the stance on short-term rates, following the recent move lower.

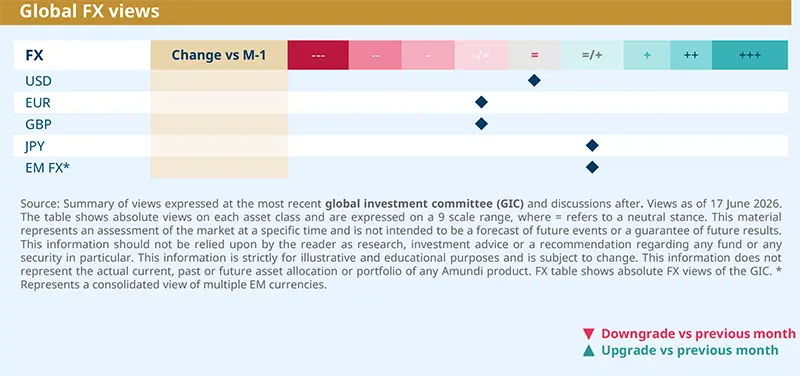

On FX, USD structural weakness is more likely over the long term; in the near term the currency could find support from a more hawkish Fed. We are positive on AUD/USD to express our bearish view on the US dollar and remain exposed to the commodity-sensitive story. We are also positive on JPY and NOK versus EUR. The yen will benefit if the economic growth environment worsens, the NOK will gain from Norway’s energy exposure.

VIEWS

Amundi views by asset classes

IMPORTANT INFORMATION

The MSCI information may only be used for your internal use, may not be reproduced or disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranty of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.mscibarra.com).

The Global Industry Classification Standard (GICS) SM was developed by and is the exclusive property and a service mark of Standard & Poor's and MSCI. Neither Standard & Poor's, MSCI nor any other party involved in making or compiling any GICS classifications makes any express or implied warranties or representations with respect to such standard or classification (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such standard or classification. Without limiting any of the forgoing, in no event shall Standard & Poor's, MSCI, any of their affiliates or any third party involved in making or compiling any GICS classification have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.

This document is solely for informational purposes. This document does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or any other product or service. Any securities, products, or services referenced may not be registered for sale with the relevant authority in your jurisdiction and may not be regulated or supervised by any governmental or similar authority in your jurisdiction. The information contained in this document must not be altered or presented in a way that could give rise to misunderstanding or misrepresentation. Any use, reproduction, or distribution of the document’s content without full and proper reference to the original source is prohibited. Any information contained in this document may not be used as a basis for or a component of any financial instruments or products or indices. Furthermore, nothing in this document is intended to provide tax, legal, or investment advice. Unless otherwise stated, all information contained in this document is from Amundi Asset Management S.A.S. and is as of 30 June 2026. Diversification does not guarantee a profit or protect against a loss. This document is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The views expressed regarding market and economic trends are those of the author and not necessarily Amundi Asset Management S.A.S. or Amundi-Acba Asset Management CJSC and are subject to change at any time based on market and other conditions, and there can be no assurance that countries, markets or sectors will perform as expected. These views should not be relied upon as investment advice, a security recommendation, or as an indication of trading for any Amundi or Amundi-Acba product. Investment involves risks, including market, political, liquidity and currency risks. Furthermore, in no event shall Amundi or Amundi-Acba have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages due to its use.

Date of first use: 30 June 2026.

"AMUNDI-ACBA ASSET MANAGEMENT" CJSC is a legal entity registered in Armenia, who, based on the Investment fund management license number 0002, provided by the Central Bank of Armenia, carries out mandatory pension fund management activities in Armenia. The registered office is located 10 Vazgen Sargsyan street, Premises 100-101, Yerevan, Armenia.

For more information about Amundi-Acba you can visit www.amundi-acba.am or call 011-310-000.