The Fed’s employment mandate taking centre stage

US bond yields have declined over the past couple of months, and gold has touched records levels. Global and US equities have also reached new highs on the back of expectations of continued economic strength in the US, the monetary easing cycle, earnings resilience, and AI-led momentum. We see an inherent contradiction here, but agree with the monetary easing aspect. The contradiction arises from the view that if the Fed implements rate cuts mainly to address a slowing economy, then the effects of a slowing economy should already be evident in weak labour markets, consumption, and eventually in corporate earnings.

The aforementioned topics, including economic growth, inflation, and monetary easing, will likely unfold as follows:

"We see one risk on monetary policy: the ECB turns out to be (over) cautious and cuts policy rates by less than what’s needed, sticking to its price stability mandate".

While we note some divergences in monetary policies, a willingness to support the economy is there. In this backdrop and when risk assets valuations are high, market volatility could present an opportunity to add risk on the more stable, quality segments of the market.

Amundi Investment Institute: ECB-Fed divergences and impact of US inflation on Europe

The divergence between the US and EU will pose dilemmas for the ECB. As the Fed continues on its path to reduce rates more aggressively than the ECB, an appreciating EUR/USD exchange rate, coupled with US tariffs, would significantly weigh on EU exports and, ultimately, on growth. At that point, the ECB will have to decide how to respond. Second, rising US inflation and higher term premia may put upward pressure on US yields at the long end of the yield curve. This could affect long-end yields in Europe as well, and may pose challenges for governments burdened with high debt and fiscal deficits.

Services constitute a larger component of the overall US CPI, so we are monitoring whether changes in goods prices (due to tariffs) will impact services. Second, companies’ ability to pass on higher goods costs to consumers depends on several micro-level factors, such as corporate pricing power, the expected extent of substitution by consumers, and the elasticity of demand. We believe a combination of price hikes and absorption of higher costs by companies is the most likely scenario.

"Although the trade agreement with the US has reduced uncertainty over tariffs, we believe that once the effects of higher tariffs begin to weigh on growth in the EU, the ECB will be prompted to cut policy rates — once this year and once in Q1 next year".

Monica DEFEND

Head of Amundi Investment Institute & Chief Strategist

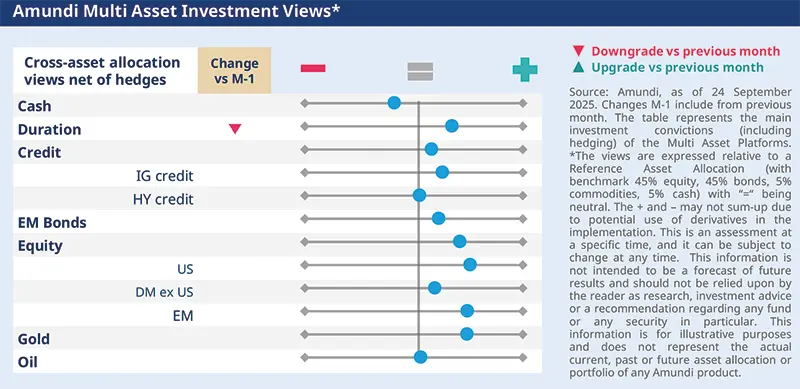

Our mildly positive risk stance is outlined across asset classes below:

"While staying positive on risk, we await signals on how AI technology could improve productivity and provide a boost to corporate margins. We prefer to play on fundamentals".

FIXED INCOME

Benefit from income potential in credit

Amaury D’ORSAY

Head of Fixed Income

We are witnessing an odd combination of slowing economic growth in the US and some risk assets reaching record levels. In the Eurozone, the impact of US tariffs and German fiscal boost on growth is yet to be seen. Amid all this, the Fed has initiated its rate cut cycle, despite no signs of recession. Even the ECB, which we expect to stay data-dependent, will likely reduce policy rates as we enter the year-end phase.

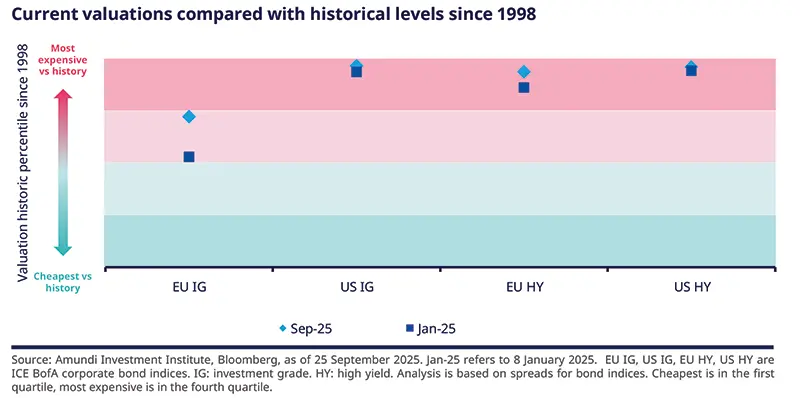

We think rate cuts by central banks could likely enhance the appeal of income-generation potential in credit markets, but investors should be mindful of valuations and quality. Hence, this is an opportune time for identifying those segments where carry is attractive and fundamentals reasonably strong.

Duration and yield curves

Corporate credit

FX

EQUITIES

A pinch of salt on AI-euphoria

Barry GLAVIN

Head of Equity Platform

US markets, and to some extent global stocks, have been led by positive newsflow around the AI theme, but we believe markets are over-optimistic on the massive capex plans around this theme. The key question is: what if something cheaper (like the ‘DeepSeek moment’) and faster emerges, and how could that affect the return on investment? Additionally, fiscal expansion and central banks cutting rates are adding to that enthusiasm. To us, this presents the biggest vulnerability.

And hence risk management is getting more important. At the same time, we are identifying granular themes such as corporate reforms in Japan, income generation in the UK, and fiscal boost in Europe (beneficial for mid and small-caps). Overall, our focus remains on quality business models and valuations.

Global convictions

Sector and convictions

EMERGING MARKETS

Emerging markets in a multi-polar world

Yerlan SYZDYKOV

Global Head of Emerging Markets

Although the US’s economic clout remains dominant, EM countries that can adapt and position themselves around new technologies (such as AI in China) and the reshaping of global supply chains (such as India) will be the beneficiaries of this shift towards multipolarity. More recently, for us, the main topic of internal debate has been the dollar weakness and how the Fed’s monetary easing and Trump’s policies and pressure could affect the currency.

From a structural perspective, EM continue to offer opportunities for selection and diversification, relatively delinked from the global cycle. Hence, we remain overall constructive with a keen focus on the Fed, EM country-specific factors, and geopolitical risks.

EM bonds

EM equities

Main convictions from Asia

Strong performance across Asian markets continues, driven by fading tariff risks and rising global risk sentiment. Trade activity has remained resilient despite tariff scares, while limited inflation is allowing Asian central banks to maintain an easing bias. Globally, the Fed’s resumption of rate cuts should keep the dollar on the back foot. A weak dollar, combined with robust investor sentiment, typically creates a favourable environment for Asian markets.

Asian assets well-positioned in a global context. Earnings forecasts for Asia remain mostly positive. Technicals and sentiment are also strong, and equity valuations remain attractive compared to developed markets. However, selectivity is crucial as market performance has been uneven. We are positive on India following recent market consolidation and solid earnings growth, while adopting a more cautious stance on Korea after its strong market re-rating.

For bonds, we expect credit spreads to continue grinding tighter, supported by a strong technical backdrop. New issuances are easily absorbed by markets, with investors continuing to hold plenty of dry powder. Lower US Treasury yields are keeping Asian bond markets well supported. However, we are closely monitoring the political and social events in Indonesia and how that has affected government bonds.

MULTI-ASSET

Fine-tune duration amid evolving inflation

Francesco SANDRINI

CIO Italy & Global Head of Multi-Asset

John O’TOOLE

Global Head - CIO Solutions

"While staying positive on duration overall, we are now neutral on UK gilts due to near-term inflation pressures and the fiscal outlook in the country".

US economic activity is likely to slow in the second half of the year due to weak consumption, which is a dominant part of the economy. We also expect some resilience in inflation in the near term. Even in the UK, the Central Bank is grappling with an uptick in price pressures. In Europe, however, the environment is slightly different in the sense that inflation is under control for now. On risk assets, while valuations are high in some segments, we maintain a slightly positive risk stance (without bold calls) led by fundamentals and earnings potential. At the other end, we reiterate the need for hedges on equities and other portfolio diversifiers/stabilisers such as gold.

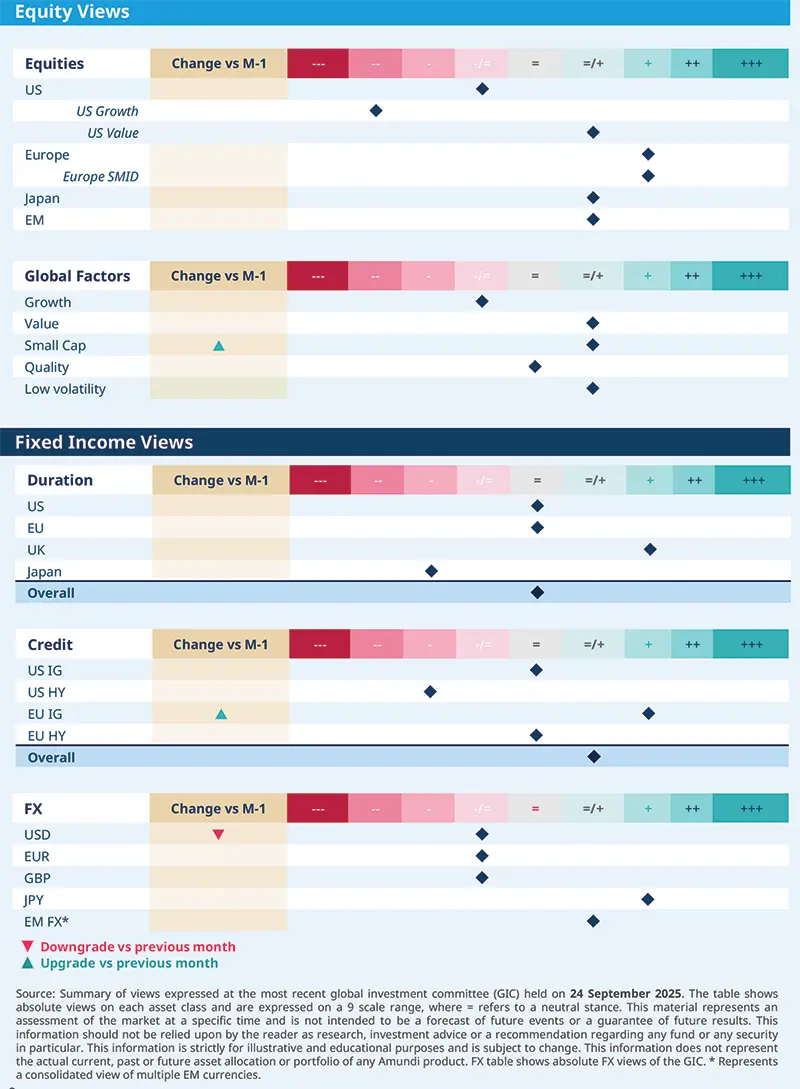

Our constructive stance on equities is maintained through the US, the UK, and emerging markets. In the US, earnings momentum, a dovish Fed, and technological advances are positive factors for the benchmark markets. But we maintain a well-diversified approach and are positive on mid-caps, which have lagged the broader markets and are mainly focused on the domestic US economy, outside of the large-cap tech sector. Furthermore, we are optimistic on EM equities in general and on China. Monetary easing by the Fed opens up room for EM central banks to boost their domestic growth environment.

We remain positive on duration overall, including on the US (5Y), and core EU and Italian BTPs vs Bunds. However, we believe UK inflation, particularly in services, is showing an upward trend, at a time when markets are increasing the scrutiny of the yet-to-be-released government budget. As such, we have tactically downgraded UK duration to neutral, and stay cautious on Japan due to valuations and expectation of a rate hike by the BoJ. In credit, we are constructive on EU IG, and on EM spreads.

In the medium term, the USD looks set to be pressured by structural factors such as high debt, allowing us to stay cautious. We are positive on EUR, JPY/EUR and in EM, we continue to favour MXY over CNY.

VIEWS

Amundi views by asset classes

IMPORTANT INFORMATION

The MSCI information may only be used for your internal use, may not be reproduced or disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranty of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.mscibarra.com).

The Global Industry Classification Standard (GICS) SM was developed by and is the exclusive property and a service mark of Standard & Poor's and MSCI. Neither Standard & Poor's, MSCI nor any other party involved in making or compiling any GICS classifications makes any express or implied warranties or representations with respect to such standard or classification (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such standard or classification. Without limiting any of the forgoing, in no event shall Standard & Poor's, MSCI, any of their affiliates or any third party involved in making or compiling any GICS classification have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.

This document is solely for informational purposes. This document does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or any other product or service. Any securities, products, or services referenced may not be registered for sale with the relevant authority in your jurisdiction and may not be regulated or supervised by any governmental or similar authority in your jurisdiction. Any information contained in this document may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. Furthermore, nothing in this document is intended to provide tax, legal, or investment advice. Unless otherwise stated, all information contained in this document is from Amundi Asset Management S.A.S. and is as of 30 September 2025. Diversification does not guarantee a profit or protect against a loss. This document is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The views expressed regarding market and economic trends are those of the author and not necessarily Amundi Asset Management S.A.S. and are subject to change at any time based on market and other conditions, and there can be no assurance that countries, markets or sectors will perform as expected. These views should not be relied upon as investment advice, a security recommendation, or as an indication of trading for any Amundi product. Investment involves risks, including market, political, liquidity and currency risks. Furthermore, in no event shall Amundi have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages due to its use. Assumptions on tariffs as of 28 August 2025, countries face value tariffs are adjusted with sectoral tariffs (Section 232) and/or exemptions. On India, 25% Universal tariffs and 25% secondary sanctions on Russian Oil Imports; on China 20% Fentanyl and 10% reciprocal. Sectoral tariffs on Canada and Mexico only for non-USMCA-compliant imports.

Date of first use: 30 September 2025. DOC ID: 4285688

Document issued by Amundi Asset Management, “société par actions simplifiée”- SAS with a capital of €1,143,615,555 - Portfolio manager regulated by the AMF under number GP04000036 - Head office: 91-93 boulevard Pasteur, 75015 Paris - France - 437 574 452 RCS Paris - www.amundi.com.